Market Notes – April 28/22

US stocks ended sharply higher Thursday, led by technology shares as markets continued a comeback from steep losses earlier this week. This gain was in spite of the news that the US economy unexpectedly contracted at the start of 2022 for the first time in nearly two years as lingering supply chain imbalances, inflationary pressures, and war in Eastern Europe weighed on growth. First-quarter US gross domestic product (GDP) fell at a 1.4% annualized rate after a 6.9% pace of growth at the end of 2021.

The bad news is good news logic here is that the Fed will be less likely to aggressively raise rates if the economy is heading toward a recession. The other spark for the markets was the anticipation for Apple’s earnings, which came in positive after the close.

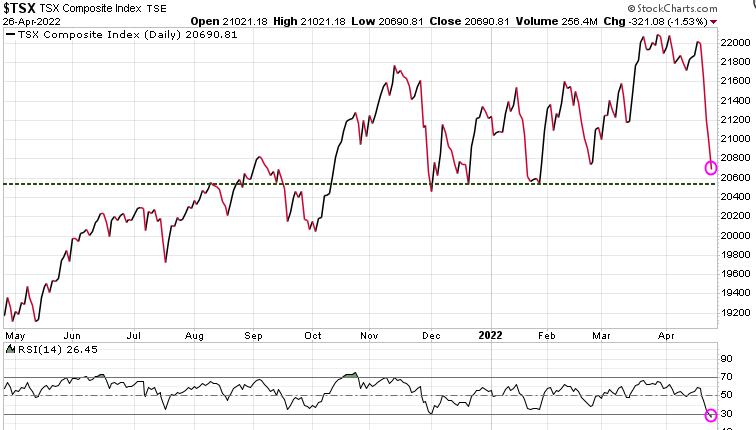

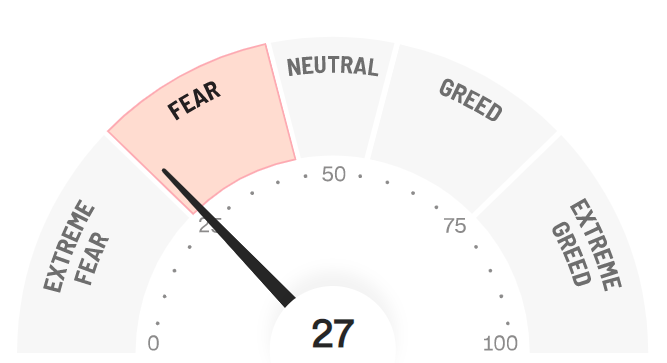

As we highlighted in Tuesday’s Today’s Charts, investor sentiment had gotten very negative (bearish) and suggested that we would see a relief rally. Right on schedule, starting Wednesday we saw the markets rally, and then today had a gonzo spike.

The key support for the S&P 500 was the 4173 level which held the previous two times it was tested (green arrows). It held again this week, which triggered this relief rally which should test near-term resistance at 4465 (light red dashed horizontal line). If it can push through that level, then the next resistance is 4630 (next red dashed horizontal line).

The S&P 500 has seen a series of lower highs and lower lows, so until it breaks out of that trend we need to be cautious here. The 4173 remains near-term support and if that level gets taken out, then we are in for a deeper correction, potentially much deeper.

The US dollar has been on a parabolic tear this year. With Exchange Traded Funds (ETFs) it is very easy to trade currencies, just as easy as trading any stock. Unfortunately, most investors miss these opportunities. Trend Letter uses these ETFs and currently has a leveraged short Euro trade that is up over 32% right now.

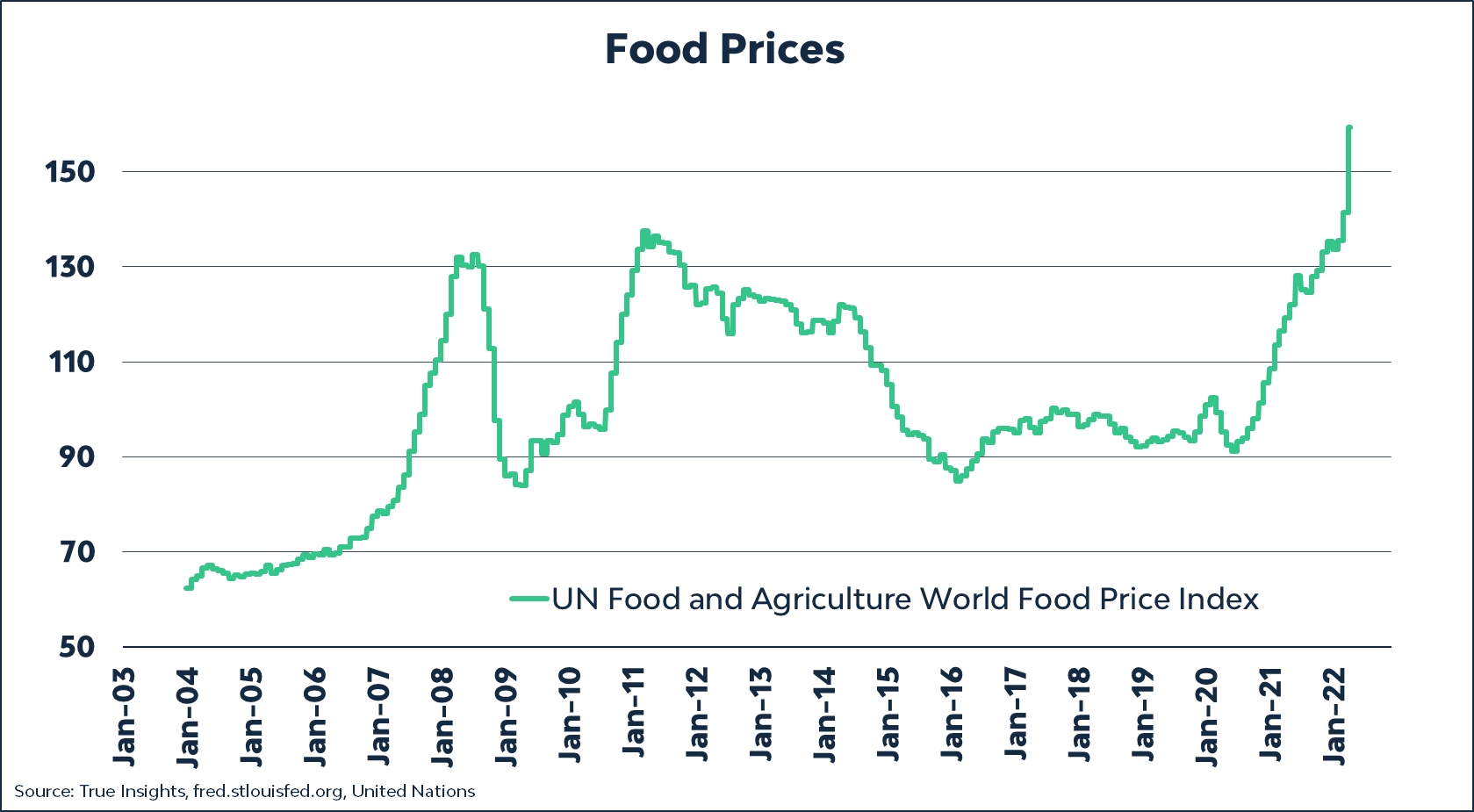

The Japanese 10-year bond yield has been negative until just recently, and even today only pays 0.21%. The US yield is 2.82% (Canada is 2.78%), so Japanese investors are pouring into US bonds, meaning they are converting Yen for $US. As a result, the Yen is getting hammered, down over 20% this year. A weak Yen drives up import costs, especially energy and food.

After hitting .83 in early June thanks to energy and commodities, the Loonie has not been able to maintain that strength due to the massive strength in the US.

Stay tuned!